In our previous blog, we explored the foundational aspects of the GHG Protocol, emphasizing its role in standardizing GHG emissions measurement across industries. Building upon that, this blog delves deeper into the core components of the GHG Protocol, specifically Scope 1, Scope 2, and Scope 3 emissions. Understanding these scopes is crucial for organizations striving to manage their carbon footprint effectively. As regulations tighten and businesses move toward sustainability, having a solid grasp of these emission categories becomes increasingly essential for accurate reporting and impactful reduction strategies.

In this blog, we will explore:

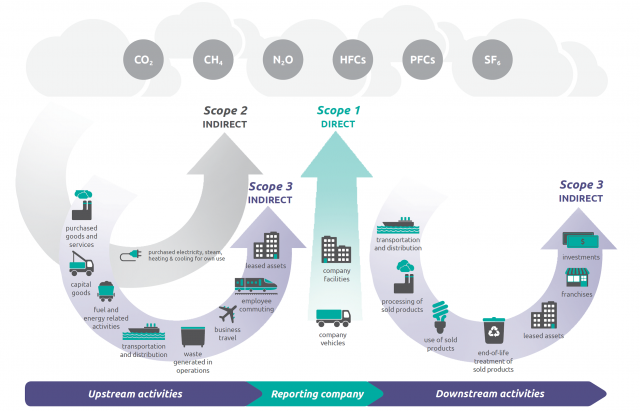

Scope 1 GHG Emissions

Scope 1 emissions encompass direct greenhouse gas emissions that originate from sources owned or controlled by the reporting organization. This includes emissions from activities such as combustion of fossil fuels in company-owned vehicles, emissions from on-site industrial processes, and emissions from owned or controlled facilities like boilers and furnaces.

Categories of Scope 1 Emissions:

- Stationary Combustion: This category includes emissions from the direct burning of fossil fuels to generate energy for heating or power in stationary equipment, such as boilers and furnaces.

- Mobile Combustion: Emissions from all vehicles owned or controlled by the organization fall under this category. This includes emissions from cars, trucks, and other vehicles that run on fossil fuels.

- Fugitive Emissions: These are unintentional releases of greenhouse gases from equipment leaks, such as those found in refrigeration and air conditioning systems. Fugitive emissions can be particularly potent, as some refrigerants have a much higher global warming potential than carbon dioxide.

- Process Emissions: This category encompasses emissions released during industrial processes and manufacturing activities. Examples include emissions generated during cement production or chemical manufacturing.

Scope 2 GHG Emissions

Definition: Scope 2 emissions consist of indirect greenhouse gas emissions that result from the generation of purchased electricity, steam, heating, or cooling consumed by the reporting organization. While these emissions occur upstream in the supply chain, they are associated with the organization’s energy consumption.

Categories of Scope 2 GHG emissions:

- Purchased Electricity: Emissions associated with electricity purchased from the grid, which may be generated from fossil fuels, renewables, or a mix of energy sources.

- Purchased Heat and Steam: Emissions connected to the consumption of heat and steam procured from external sources, such as district heating systems.

Scope 3 GHG Emissions

Scope 3 GHG emissions refer to all indirect greenhouse gas emissions associated with an organization’s value chain that occur from sources outside its direct control. These emissions extend beyond the organization’s operational boundaries. In this article, we will explore the 15 categories of Scope 3 emissions as defined by the GHG Protocol, providing insights into their significance and how they can influence your sustainability objectives.

- Purchased Goods and Services: This category includes all emissions from the production of goods and services that a company purchases. It covers the extraction, production, and transportation of these goods and services. For many industries, this is one of the largest sources of Scope 3 emissions, especially for sectors heavily reliant on supply chains.

- Capital Goods: Emissions in this category come from the production of capital goods such as machinery, equipment, and buildings. Capital goods typically have long life cycles, but their manufacturing can involve significant energy and raw material usage.

- Fuel- and Energy-Related Activities (Not Included in Scope 1 or 2): These emissions include the upstream lifecycle emissions from fuels and energy purchased and consumed by the organization. For example, emissions from the extraction, refining, and transportation of the fuels that the company uses fall under this category.

- Upstream Transportation and Distribution: This category covers emissions from the transportation and distribution of products purchased by the company in vehicles not owned or controlled by the company. It includes the movement of goods from suppliers to the company’s facilities.

- Waste Generated in Operations: Emissions from the disposal and treatment of waste generated by a company’s operations, such as solid waste and wastewater, are included here. The more waste a company generates, the higher its emissions in this category, particularly if the waste management methods involve landfilling or incineration.

- Business Travel: This category includes emissions from business travel in vehicles not owned or controlled by the reporting company, such as flights, trains, and car rentals. For companies with a global workforce, business travel can be a significant contributor to Scope 3 emissions.

- Employee Commuting: Emissions from the transportation used by employees to travel to and from work fall under this category. It includes emissions from personal vehicles, public transit, and any other commuting methods.

- Upstream Leased Assets: If a company leases assets (such as offices or vehicles) that are not included in Scope 1 and Scope 2, the emissions associated with operating these assets fall under Scope 3. This category applies to leased assets that the company does not directly control.

- Downstream Transportation and Distribution: This category captures emissions from the transportation and distribution of products sold by the reporting company between its operations and the end consumer, if not already included in Scope 1 and Scope 2.

- Processing of Sold Products: Emissions associated with the processing of intermediate products sold by a company to another company are captured here. For instance, if a company sells steel to an automaker, the emissions from processing that steel into a finished vehicle would fall under this category.

- Use of Sold Products: This category includes the emissions from the use of products sold by the company. For example, the combustion of fossil fuels by consumers, such as gasoline used in cars or natural gas used for heating, would be captured here.

- End-of-Life Treatment of Sold Products: When products reach the end of their life and are discarded, emissions are generated from their treatment, including recycling, incineration, or landfilling. This category includes emissions from all methods of disposal used by consumers or downstream industries.

- Downstream Leased Assets: Emissions from leased assets that the company has leased to other entities are accounted for here. For example, if a company leases equipment or real estate to another company, the emissions from the energy use of those assets are captured in this category.

- Franchises: Franchises are a significant category for businesses operating on a franchise model. This category includes emissions from franchise operations that are not under the direct control of the reporting company but are part of its overall business strategy.

- Investments: For financial institutions, investments can be a major source of Scope 3 emissions. This category captures emissions associated with the company’s investments in assets, such as stocks, bonds, and other financial products. The carbon footprint of these investments can be considerable, especially if the invested companies operate in carbon-intensive industries.

By categorizing GHG emissions in this way, organizations can identify key areas for improvement, set targeted reduction goals, and ultimately contribute to a more sustainable future. Addressing all GHG scopes not only helps mitigate climate change but also enhances corporate reputation and operational efficiency. Embracing this holistic approach to emissions management is vital for achieving long-term sustainability objectives.

Stay tuned for the next blog, where we will explore about ghg protocol and other emission accounting methodologies for achieving sustainability goals. Together, let’s work towards a more sustainable future!