An Indian steel exporter spent most of 2025 getting their EU CBAM data right. They worked through the emissions calculations, got their installation-level data in order, and came into 2026 with verified figures their European buyers could use. It was a significant effort. It is also not transferable to what comes next. The UK will introduce its own CBAM from 1 January 2027, covering aluminium, cement, fertilisers, hydrogen, iron and steel. For any Indian exporter shipping to both the EU and the UK, that is not an extension of existing compliance. It is a separate mechanism with different thresholds, different pricing logic, different reporting timelines, and a different administrative body. The work done for Brussels does not automatically satisfy the rules being set in London. A CBAM Consultant who has worked through EU compliance with an Indian exporter already knows their emissions data. Starting UK CBAM preparation with that foundation is faster. Starting without a CBAM Consultant, assuming the EU work covers it, is where exporters run into problems.

What a CBAM Consultant Finds When Comparing EU and UK CBAM Requirements

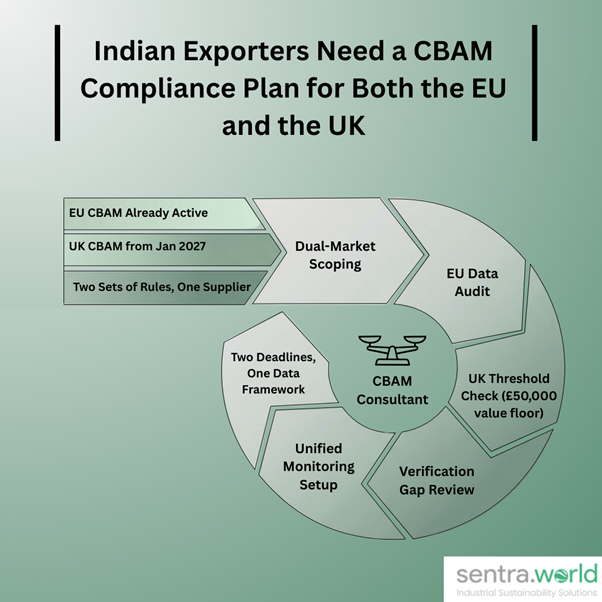

The two regimes share the same underlying goal, placing a carbon cost on imports to prevent carbon leakage, but the mechanics differ in ways that matter practically. The EU CBAM uses a certificate system where importers purchase and surrender certificates priced against the weekly average of EU ETS allowances. The UK CBAM operates more like a tax return, using sector-specific levy rates adjusted quarterly based on the UK ETS and Carbon Price Support, not a certificate market. The compliance process, the registry, and the payment mechanism are all different. The thresholds differ too. The EU exempts importers bringing in under 50 tonnes of CBAM-covered goods per year. The UK threshold is set at £50,000 of CBAM goods imported over a 12-month period, a financial floor rather than a weight-based one. An Indian exporter shipping smaller volumes of high-value steel products to the UK may clear the EU’s 50-tonne threshold but exceed the UK’s £50,000 value threshold, or vice versa. A CBAM Consultant maps exactly where each exporter sits against both thresholds before any registration or compliance work begins. The reporting calendar is also different. EU importers submit annual CBAM declarations by 30 September each year. UK importers will submit their first annual CBAM return covering the whole of 2027 by May 2028, after which the system moves to quarterly returns from 2028 onwards. Two deadlines, two registries, two sets of data requirements running in parallel for any exporter active in both markets.

Why EU-Verified Emissions Data Does Not Automatically Satisfy UK CBAM Requirements

This is the assumption most Indian exporters make, and it is the one a CBAM Consultant corrects early. The emissions data built for EU CBAM is calculated under EU Implementing Regulation 2023/1773 and verified by an ISO 14065-accredited body against EU ETS methodology. The UK is developing its own verification framework aligned to IAF-accredited bodies such as UKAS. Emissions data for UK CBAM must be verified by an accredited body, and the UK government has indicated that default values will apply where verified data is not available, with those defaults set for an initial period of 2027 to 2030. The practical implication: an Indian exporter with verified EU emissions data may still need separate verification for UK CBAM purposes, depending on whether their existing verifier holds the relevant UK accreditation. At the UK-EU Summit in May 2025, both parties committed to exploring mutual exemptions and harmonising reporting methodologies, but those talks have not yet produced formal alignment. Until they do, Indian exporters shipping to both markets need a compliance infrastructure that covers both sets of rules independently. A CBAM Consultant reviews whether existing EU-verified data can be adapted for the UK submission or whether a separate verification process is required, and identifies which elements of the exporter’s current monitoring setup need to be extended to satisfy UK requirements.

How a CBAM Consultant Builds a Dual-Market Compliance Plan for Indian Exporters

For Indian exporters active in both the EU and UK markets, the most efficient approach is building a compliance structure that serves both mechanisms from the same underlying emissions data, where the rules permit it. A CBAM Consultant structures that in three steps:

- Auditing the existing EU emissions dataset to identify which elements of the calculation, system boundary, and activity data would satisfy UK CBAM methodology requirements, and where gaps exist that require additional data collection before January 2027.

- Confirming UK CBAM registration obligations based on the £50,000 annual import value threshold, identifying which UK buyers will cross that threshold and therefore need verified data from the Indian supplier to avoid UK default values.

- Setting up the monitoring and documentation framework so that the same installation-level emissions data feeds both the EU annual declaration and the UK CBAM return without duplicating the measurement effort at the production facility level.

India’s steel and aluminium exports reach both Amsterdam and Birmingham. The compliance calendar now runs to two separate deadlines, two separate registries, and two separate sets of rules. The exporters who treat them as one problem will find that out when the UK deadline arrives. A CBAM Consultant builds the plan that covers both before either deadline becomes urgent.