India’s carbon policy is undergoing its most significant structural shift in over a decade -and for industrial operators, the stakes have never been higher. The Carbon Credit Trading Scheme (CCTS) marks India’s transition from a voluntary energy-efficiency program to a mandatory, market-based compliance framework, fundamentally redefining how heavy industry accounts for its emissions.

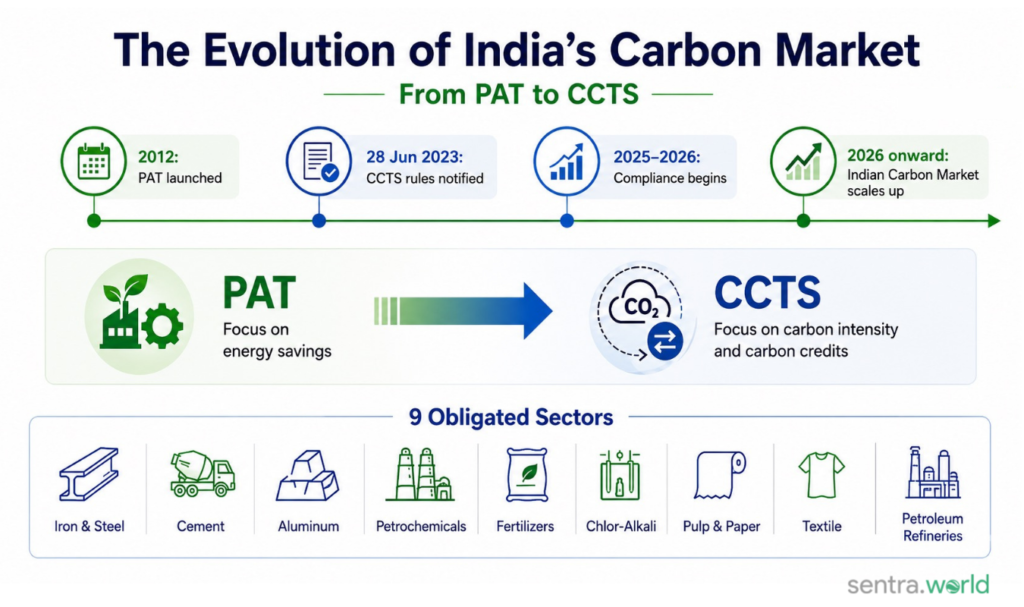

The story begins with the Perform, Achieve, and Trade (PAT) scheme, launched in 2012 under the National Mission for Enhanced Energy Efficiency. PAT required designated energy-intensive industries to reduce their specific energy consumption, rewarding over-achievers with tradable Energy Saving Certificates (ESCerts). While PAT delivered measurable gains, its narrow focus on energy intensity left greenhouse gas emissions largely unaddressed.

CCTS replaces energy savings with carbon intensity as the governing metric meaning obligated entities must now reduce CO₂ equivalent emissions per unit of output, not just kilowatt-hours consumed. This change aligns India’s domestic framework with international carbon market standards and positions the country’s industrial sector within a credible decarbonization pathway ahead of its 2070 net-zero target.

The Bureau of Energy Efficiency (BEE) sits at the center of this architecture as the designated administrator, responsible for setting sector-specific targets, issuing Carbon Credit Certificates (CCCs), and overseeing compliance. According to BEE’s own reporting, the scheme will initially cover CCTS India compliance sectors including aluminum, cement, chlor-alkali, iron and steel, paper and pulp, petrochemicals, and textiles -affecting over 1,000 industrial units transitioning from PAT.

| Milestone | Timeline |

| CCTS Rules notified | 28/06/2023 |

| Compliance obligations enter force | 28/06/2023 |

| Full Indian Carbon Market (ICM) operational target | 2026 onward |

The 9 Obligated Sectors Under CCTS India Compliance

The CCTS compliance framework applies to 9 energy-intensive sectors -and understanding whether your industry falls inside the net is the first step toward building a response strategy.

The Indian Carbon Market guidelines designate the following sectors as obligated entities:

- Iron & Steel

- Cement

- Aluminum

- Petrochemicals

- Fertilizers

- Chlor-Alkali

- Pulp & Paper

- Textile

- Petroleum Refineries

Any industrial unit within these sectors that meets the notified energy consumption threshold is legally required to participate. There is no opt-in provision.

Hard-to-abate sectors carry disproportionate weight in this framework. Iron and steel, cement, and aluminum account for a significant share of industrial emissions because their production processes rely on high-temperature heat and chemical transformation, not just electricity consumption. For these sectors, compliance will demand capital investment, process redesign, and long-term abatement planning.

Energy and processing sectors face equally complex transitions. Petroleum refineries, for example, operate integrated systems where emissions reductions in one process can shift energy burdens elsewhere. Under CCTS, that complexity becomes visible in the carbon intensity calculation -and it creates both risk and opportunity for operators who can optimize across the full facility.

CCTS Compliance for the Steel Industry: Primary vs. Secondary Producers

The steel sector faces the most complex compliance structure under CCTS because “steel producer” captures facilities with radically different production routes, emissions profiles, and data maturity levels.

Integrated Steel Plants vs. Secondary Producers

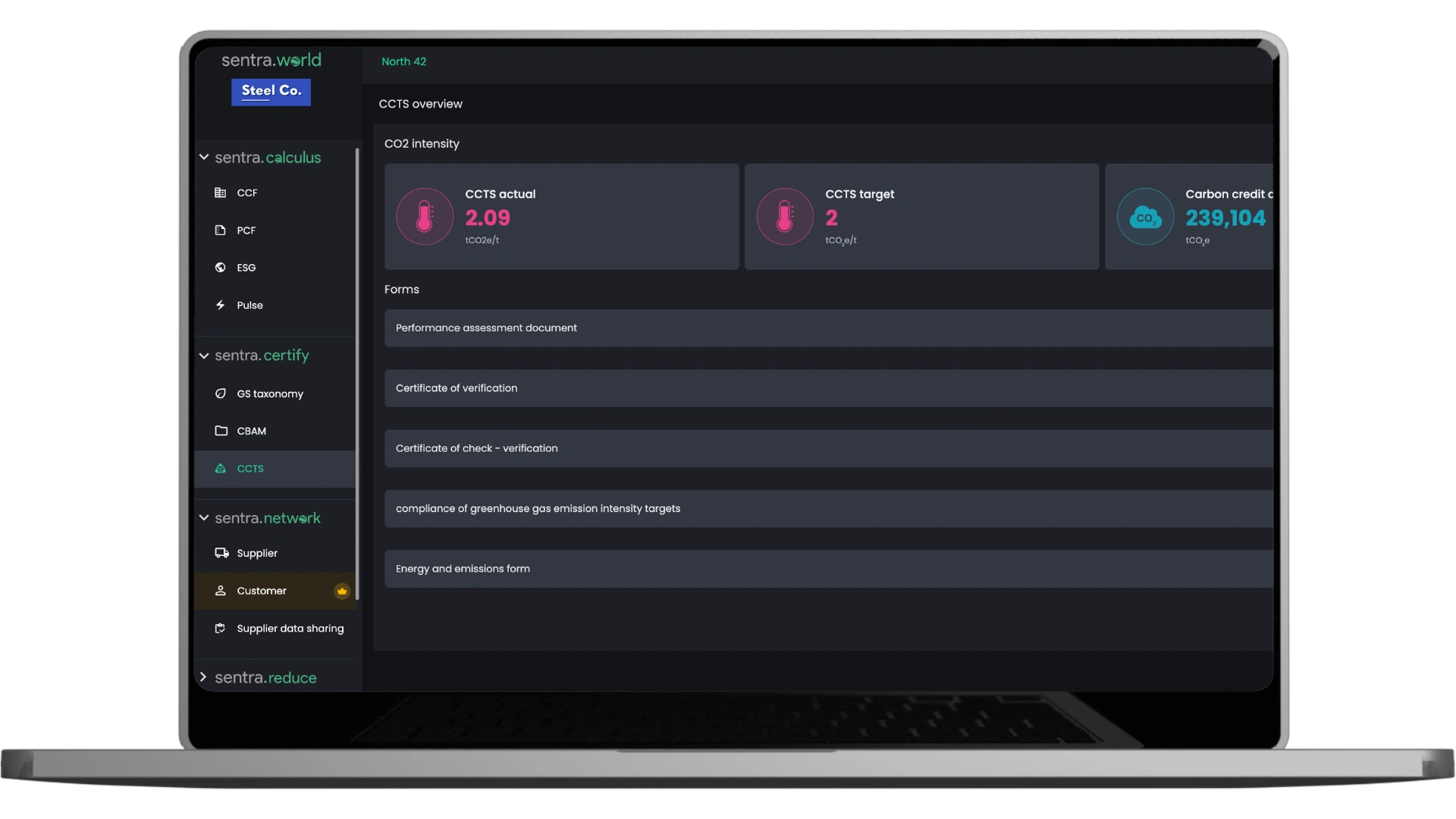

Integrated Steel Plants (ISPs), which use the blast furnace/basic oxygen furnace route, operate at massive scale with sophisticated energy monitoring infrastructure. Their ore-based production is inherently carbon-intensive, with emission intensities typically ranging 2.0–2.5 tCO₂ per tonne of crude steel. These facilities generally have the internal resources to meet CCTS data collection requirements.

By contrast, secondary producers using electric arc furnaces (EAFs) and scrap-based inputs operate at significantly lower emission intensities, often below 0.8 tCO₂ per tonne -a structural advantage that directly shapes their intensity targets under the scheme.

This distinction matters enormously for CCTS compliance for secondary steel producers India, because the BEE sets sector-specific benchmarks that account for production route. Scrap-based producers start from a lower baseline, meaning their assigned intensity targets reflect that advantage – but it also means the margin for credit generation is tighter unless efficiency gains are significant.

MSME Steel Units: The Data Challenge

MSMEs represent a large share of India’s secondary steel ecosystem, yet data collection remains their most acute compliance barrier. Many smaller re-rollers and induction furnace operators lack automated metering systems, making it difficult to produce the granular production and energy consumption records that CCTS verification demands.

Building robust monitoring systems is a prerequisite -not an afterthought -for compliance readiness. Investing in carbon measurement systems early reduces audit risk substantially.

Turning Compliance Into ‘Green Steel’ Branding

Secondary producers who achieve verified low-intensity performance under CCTS hold a genuine commercial asset: independently audited proof of greener production. As Abhay Bakre, former Director General of BEE, stated: “The CCTS will provide a market-based mechanism to incentivize the adoption of low-carbon technologies in India’s hard-to-abate sectors.”

For scrap-based producers, that incentive translates directly into Green Steel positioning for export customers -particularly relevant given evolving EU carbon border requirements that reward verifiable low-emission supply chains.

Understanding compliance obligations is only part of the picture -the next critical question is how carbon credits are calculated once production data is in hand.

The Math of Decarbonization: Calculating Carbon Credits in CCTS India

Under CCTS, your credit position is determined by a single core formula -and getting the inputs wrong can cost you significantly more than the credits themselves.

Understanding how to calculate carbon credits for the steel industry in India, or any other obligated sector, starts with one straightforward equation: (Assigned Intensity − Achieved Intensity) × Production Volume. According to the Ministry of Power’s CCTS notification, credits are issued to entities that perform better than their assigned intensity target, measured in tonnes of CO₂ per tonne of product.

If your plant emits less per unit of output than the Bureau of Energy Efficiency (BEE) mandates, the surplus translates directly into tradeable Indian Carbon Credit (ICC) certificates.

Example Scenario: Crude Steel Producer

| Variable | Value |

| Assigned Intensity Target | 2.10 t CO₂ / t steel |

| Achieved Intensity | 1.85 t CO₂ / t steel |

| Outperformance | 0.25 t CO₂ / t steel |

| Annual Production Volume | 500,000 tonnes |

| Credits Generated | 125,000 ICC certificates |

Each ICC certificate represents 1 tonne of CO₂ equivalent avoided.

Baseline years are the foundation of calculation accuracy. The assigned intensity target is not arbitrary -it is derived from historical performance data across a defined baseline period. CCTS also accounts for all major greenhouse gases, not just CO₂, with emissions converted into CO₂ equivalent using standard global warming potential multipliers. Before any performance data reaches the BEE portal, an Accredited Carbon Verifier must independently audit the metering, recordkeeping, and arithmetic behind the intensity figure, making clear documentation critical to avoiding downward revisions.

Indian Carbon Market : CCTS Compliance Timelines and Reporting Obligations

Getting your compliance calendar wrong under CCTS isn’t a paperwork problem -it’s a financial liability that compounds with every missed deadline.

As the 9 sectors under CCTS move through their first formal compliance period, understanding the rhythm of annual obligations is now a core operational requirement, not a back-office task.

Annual compliance follows a structured, multi-step cycle:

- Baseline year data submission: Obligated entities report energy consumption and production output to the Bureau of Energy Efficiency (BEE) portal, establishing the intensity benchmark against which performance is measured.

- End-of-period performance reporting: At the close of each compliance period, entities submit verified emissions intensity data. Third-party verification by an accredited agency is mandatory before submission.

- Credit reconciliation deadline: Entities that finish a period above their assigned intensity target must purchase sufficient Carbon Credit Certificates (CCCs) to cover the shortfall.

- Annual compliance declaration: A formal declaration confirming credit positions are balanced must be filed through the BEE portal before the stated cutoff.

In practice, the verification and submission phases are where most delays occur. Engaging an accredited verifier early -ideally six months before the deadline -is the most reliable way to avoid bottlenecks. Understanding how intensity targets translate into credit positions before the period closes gives finance and operations teams the lead time to act.

⚠️ Penalty Warning: Non-compliance under the Energy Conservation (Amendment) Act carries financial penalties scaled to the severity and duration of the breach. Repeat violations can trigger heightened regulatory scrutiny across all PAT and CCTS obligations simultaneously.

Once your compliance position is confirmed and credits are transacted, every certificate issued and transferred is recorded in a centralized system -which leads directly to how the Indian Carbon Market Registry functions as the backbone of the entire scheme.

The Role of the Indian Carbon Market (ICM) Registry

The ICM Registry is the backbone of India’s carbon credit infrastructure -every certificate issued, transferred, or retired under CCTS flows through a single, centralized system.

As established in the previous sections, meeting carbon intensity targets India sets for obligated entities is only half the compliance equation. The other half is ensuring those reductions are accurately recorded, verified, and tradeable.

Institutional ownership matters here. Per the Ministry of Power Notification, the Bureau of Energy Efficiency (BEE) serves as the market administrator, while the Grid Controller of India (GCI) operates the registry -tracking every Carbon Credit Certificate (CCC) from issuance through retirement. No CCC exists outside this system.

How the registry process works, Step by Step:

- Account Registration: Obligated entities apply to open a registry account with the GCI, submitting entity details, sector classification, and designated signatory credentials.

- Verification & Issuance: Following third-party verification of energy performance data, BEE reviews the audit and instructs GCI to issue CCCs directly into the entity’s registry account.

- Transfer & Trading: CCCs can be transferred between registered accounts on approved exchanges -with every transaction logged in real time on the registry ledger.

- Surrender & Retirement: Entities with a deficit surrender purchased CCCs against their compliance obligation; retired certificates are permanently cancelled in the registry to prevent reuse.

Market integrity depends on this architecture. One of the registry’s most critical functions is preventing double-counting. Each CCC carries a unique serial number, and the system applies corresponding adjustments to India’s national inventory before any credit is authorized for international transfer, ensuring the same tonne of reduction isn’t claimed by two parties simultaneously.

Strategic Benefits: Turning Compliance into Green Assets

CCTS compliance isn’t just about avoiding penalties -for manufacturers who move early, it’s a mechanism for generating revenue, accessing cheaper capital, and winning global business.

As noted by the Bureau of Energy Efficiency, “the scheme is designed to make green investments financially viable for heavy industries by allowing them to monetize their emission reductions.” CCTS rewards over-performance, not just compliance.

Monetizing Over-Achievement Through CCC Sales

When a facility reduces emissions below its assigned target, the surplus translates directly into Carbon Credit Certificates (CCCs) that can be sold on the exchange. In practice, this means efficient plants don’t just avoid penalties – they generate a new revenue stream.

Preparing for the EU’s Carbon Border Adjustment Mechanism (CBAM)

Indian exporters shipping steel, aluminum, fertilizers, or cement into Europe face a direct cost under CBAM based on their embedded carbon intensity. Manufacturers already operating under a rigorous domestic compliance framework – with verified emissions data and a proven reduction trajectory are far better positioned to understand CBAM’s financial impact and minimise that exposure.

Attracting Global Buyers Seeking Low-Carbon Supply Chains

Multinational corporations under Scope 3 pressure from their own regulators and investors are actively auditing supplier emissions. A manufacturer with documented CCC issuances, third-party verified reduction data, and an active presence in the ICM Registry offers something concrete – not just a pledge.

Of course, capturing these benefits depends on getting the operational fundamentals right -and that’s where many manufacturers encounter unexpected friction.

CCTS India : Challenges in Implementation for Manufacturers

CCTS compliance exposes a critical operational gap: most industrial facilities were simply not built to track, verify, and trade carbon data at the granularity the scheme demands.

As explored in previous sections, CCTS introduces strategic opportunities -but capturing those opportunities requires overcoming four interconnected implementation challenges that trip up even well-resourced manufacturers.

Data remain the most pervasive barrier. Factories typically track energy consumption across departments using disconnected systems – utility bills, manual meter readings, and spreadsheet logs that rarely communicate with each other. Without integrated data infrastructure, manufacturers can’t reliably calculate their carbon intensity baseline – let alone monitor it in real time.

Verification risk adds to the data problem. Manual spreadsheets introduce transcription errors, formula inconsistencies, and version-control failures that Accredited Carbon Verifiers (ACVs) will flag immediately during audits.

Market volatility adds a financial planning layer that most plant managers haven’t previously navigated. Carbon credit prices under CCTS will fluctuate based on policy signals, sectoral cap adjustments, and broader market sentiment, making it difficult to forecast the ROI of decarbonization investments with confidence.

Technical capacity gaps are perhaps the least visible but most limiting challenge. Carbon accounting under CCTS draws on specialized skills -emissions factor selection, boundary setting, and methodology interpretation -that fall outside traditional engineering or finance teams’ expertise.

Addressing these challenges systematically isn’t just a compliance necessity; it’s where technology-driven solutions become decisive -a topic the next section covers in depth.

Conclusion: Preparing Your Facility for the Indian Carbon Market

The window to establish a credible carbon baseline before CCTS compliance deadlines arrive is narrowing -and the facilities that act now will dictate the competitive landscape for years to come.

India’s Carbon Credit Trading Scheme is not a distant regulatory exercise. With compliance obligations already entering force across nine designated sectors, the shift from voluntary sustainability commitments to mandatory, auditable performance targets is underway. The cost of waiting is asymmetric: facilities that delay baseline measurement face compressed timelines, higher credit procurement costs, and limited ability to influence how targets are set for their operations.

This is precisely where purpose-built technology closes the gap. sentra.world – the #1 Carbon Accounting Platform for Industrial Manufacturing – is designed around the Measure, Mitigate, and Monetise framework that CCTS demands. From automated intensity calculations and BEE-aligned reporting to credit portfolio management, sentra.world consolidates what would otherwise require multiple disconnected tools and manual reconciliation.

Ready to know exactly where your facility stands? Take a CCTS compliance readiness assessment with sentra.world and transform your carbon obligations into a measurable competitive edge.