Indian manufacturers can no longer settle for merely checking boxes in ESG reporting. With the SEBI BRSR Framework becoming more assurance-driven, companies now need tangible evidence, reliable data systems and audit-ready disclosures.

Previously, companies followed a “comply or explain” model: disclose what was possible and justify what wasn’t. This approach is evolving. BRSR Core Assurance sets a new standard with nine specific ESG attributes that require independent, reasonable assurance. It’s akin to the difference between claiming your product’s quality and having an external party verify it.

The key shift is that BRSR Core Assurance focuses on critical ESG indicators extracted from the broader SEBI BRSR Framework. While the full Business Responsibility and Sustainability Report allows wider narrative disclosure, BRSR Core requires structured, verifiable and assurance-ready ESG data.Curious about its implementation? Explore this framework to understand its implications for listed companies.

The implementation timeline is underway. According to SEBI Circular SEBI/HO/CFD/CFD-SEC-2/P/CIR/2023/122, a phased “Glide Path” begins with the top 150 listed entities, extending to the top 1,000 by FY 2026-27.

Table of Contents

SEBI Glide Path Timeline

- FY 2023-24: Top 150 listed entities – reasonable assurance required

- FY 2024-25: Top 250 entities

- FY 2025-26: Top 500 entities

- FY 2026-27: Top 1,000 entities

For Indian companies, this means ESG teams must move from manual data collection to structured Sustainability Reporting (BRSR) systems. Every reported number should be backed by source documents, calculation notes, ownership, approvals and audit trails.

For industrial manufacturers, especially those with intricate supply chains and significant emissions, the stakes are substantial. These companies face challenges related to data gaps and the costs associated with non-compliance. Identifying which of the nine ESG attributes auditors will scrutinize first is imperative.

The 9 ESG Attributes: Key Focus of BRSR Core Assurance

BRSR Core Assurance targets nine essential ESG attributes that require independent verification rather than a cursory internal review.

Understanding this focus is crucial for those serious about BRSR reporting in India. While the full BRSR framework encompasses a broad spectrum of disclosures, BRSR Core Assurance zeroes in on metrics that investors, regulators, and partners scrutinize closely. As per SEBI’s framework, these nine attributes necessitate reasonable assurance, akin to financial audits:

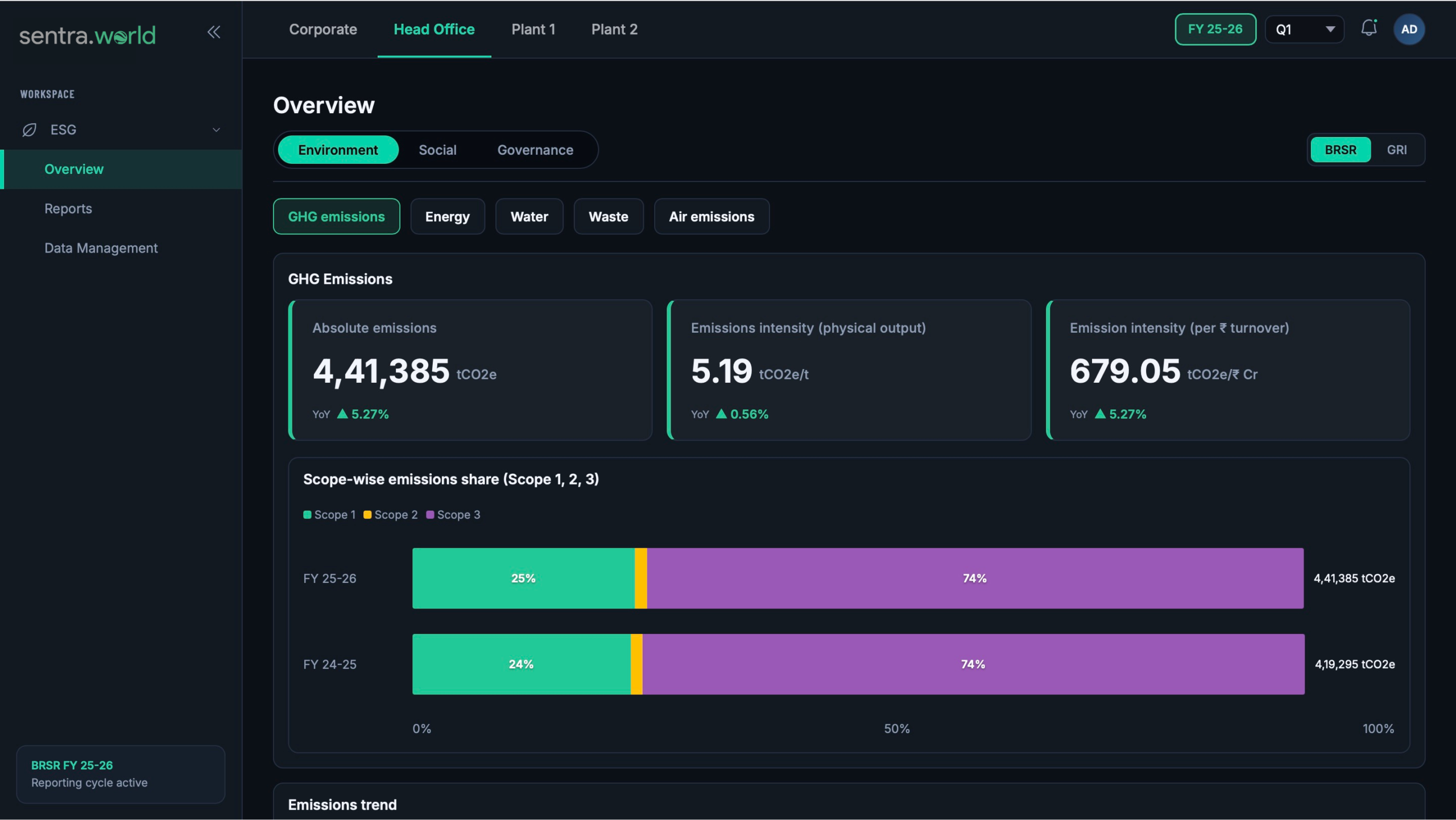

Intensity metrics are crucial for manufacturers. Absolute figures provide part of the narrative, but intensity ratios -like emissions per ton of steel are what auditors use for benchmarking. For heavy industries, these ratios connect internal data to external standards.

The distinction between reasonable assurance and limited assurance is significant. Limited assurance checks for conspicuous errors, whereas reasonable assurance demands robust evidence confirming the data’s accuracy. This entails detailed data trails, precise measurement systems, and verifiable calculations. For manufacturers with complex operations, this is where many compliance efforts encounter challenges. The nine attributes under BRSR Core Assurance require reasonable assurance, affecting sectors where emission intensity is under global scrutiny.

The Steel Sector’s Liability: Emission Intensity and Global Trade

Accurate emission data is more than a compliance requirement for Indian steel producers, it’s essential for market access and export revenue.

India’s steel industry faces a significant challenge with emission intensity. According to iFOREST research, India’s emission intensity is 2.54 tCO2 per tonne of steel, approximately 33% higher than the global average of 1.91 tCO2. This is not merely an environmental concern; it becomes a financial issue each time steel crosses a border.

The EU’s Carbon Border Adjustment Mechanism (CBAM) underscores this liability. Importers into the EU must pay for the carbon in products like steel. The EU’s carbon border policy bases duties on verified emission data, which is where SEBI BRSR Core Assurance plays a role. The nine ESG attributes, such as Scope 1 and Scope 2 GHG emissions, provide the data needed for accurate CBAM declarations. Without verified data, manufacturers may face default values or rejection by EU customs.

Unverified data poses financial risks. Without audit-grade assurance, trading partners and EU importers use conservative estimates, inflating a product’s carbon cost and affecting competitiveness. However, with verified, assured emission data, manufacturers can demonstrate a lower carbon footprint than default benchmarks suggest. Verified data becomes a valuable asset, influencing costs for buyers in high-tariff markets. For Indian exporters dealing with CBAM requirements for ferro alloys and steel, this distinction could save millions in avoided carbon costs annually.

The impact extends beyond the factory, it reverberates through supply chains, altering how large manufacturers evaluate their vendors.

While BRSR is India’s primary ESG disclosure requirement for listed companies, many businesses also align with global ESG frameworks such as GRI, IFRS S1, IFRS S2, TCFD, SASB and CDP. These frameworks are especially relevant for companies with global investors, export customers, multinational buyers or international subsidiaries.

The Value Chain Ripple Effect: MSMEs Must Prepare Now

ESG disclosures are no longer exclusive to large companies – they’re becoming essential for every supplier in the ecosystem.

This insight captures the essence of the issue. SEBI’s framework mandates the top 250 listed entities to report on ESG performance for at least 75% of their value chain by procurement value. Large companies like Tata and JSW require verified data from their vendors. This pressure cascades down to MSME suppliers.

For smaller manufacturers, the risks are tangible:

- Vendor delisting: Buyers now evaluate vendors based on ESG readiness. Suppliers without auditable data risk losing contracts.

- Delayed payments and audits: ESG disclosure clauses in agreements can trigger audits that MSMEs may not be prepared for.

- Export chain exclusion: CBAM and similar trade rules heighten this pressure; learn more about how emissions affect exporters.

ESG compliance extends beyond regulatory requirements – it’s a critical component of B2B relationships. MSMEs ignoring it will experience its impact in their order books, not just from regulators. The strategy is to establish data infrastructure before a buyer audit necessitates it – which the next section addresses.

Data Quality Best Practices: Building an Audit-Ready Infrastructure

Preparing for an audit isn’t a last-minute task -it’s about consistent data governance throughout the year.

With value chain reporting for BRSR Core mandatory for the top 250 listed entities by FY 2024-25, the need for traceable, defensible data is more pressing than ever. A robust ESG data infrastructure differentiates companies that pass assurance from those scrambling to address issues.

1. Move away from Excel to automated data collection. Spreadsheets can introduce errors and gaps -precisely what auditors target. Automated tools capture data directly from meters and systems, minimizing risks from manual entry. According to BRSR Core Assurance guidance, data traceability is a frequent failure point in assurance reviews.

2. Establish an unbroken audit trail. Each data point should trace back to a primary source, such as an invoice or meter reading. Auditors test this chain, and if a number can’t be traced, it can’t be verified.

3. Conduct internal pre-assurance checks. Before the assurer arrives, perform a structured review against your assurance checklist. This helps identify inconsistencies and gaps early.

4. Standardize emission factors and unit conversions. Different facilities using different factors is a common error. Centralizing these ensures consistency across sites and times.

Pro-tip: Schedule your internal pre-assurance review at least 60 days before the assurer’s visit. This allows time to address data gaps without rushing.

Building this infrastructure is an ongoing process, not a one-time fix. The next section offers a practical checklist for readiness.

The Bottom Line: Your BRSR Core Readiness Checklist

Understanding BRSR Core Assurance explained in a presentation is one thing, implementing it operationally is another. With SEBI’s glide path in motion, manufacturers need a framework for self-assessment before an assurer arrives.

Your audit readiness is only as robust as your weakest data link.

- Know your glide path position. Determine if your company is among the Top 150, 250, 500, or 1,000 listed entities by market cap. Your assurance timeline is based on this.

- Map your value chain exposure. Identify suppliers covering your top 75% of procurement. These relationships define your Scope 3 boundary and disclosure obligations.

- Audit your GHG accounting against the 9 Core attributes. Cross-check your emissions data with the SEBI BRSR Core framework to detect gaps before audits do.

- Engage your assurer early. As Deloitte India notes, reasonable assurance requires deeper testing than limited assurance -starting late leaves little room for corrections.

- Replace manual tracking with automated accounting. Spreadsheets can’t deliver the evidence or metrics needed for top-level assurance. The question isn’t if you should switch -it’s how quickly.

Manufacturers that begin preparations now will transform compliance into a competitive advantage tomorrow.The next section explores how automation can expedite this transition.

Automating Assurance: How sentra.world Simplifies BRSR Core

Bridging the gap between raw data and investor-grade assurance is where many manufacturers lose credibility and where technology can make a difference.

sentra.world an AI-driven sustainability platform tailored for industrial manufacturing, designed to convert fragmented data into audit-ready ESG disclosures. Instead of adapting generic tools, sentra.world addresses the unique measurement challenges of the sector.

- Automated ESG Data Collection: Gather ESG data from plants, ERP systems, Excel files, EHS records, suppliers and more.

- ESG Data Management Platform: Centralize ESG data across facilities, departments, suppliers, business units, and reporting periods.

- Framework and Standards Mapping: Map one ESG dataset to BRSR, BRSR Core, GRI, ISSB, ADX, DFM, MSX, CSRD, ESRS, customer questionnaires, and internal ESG dashboards.

- Carbon Accounting Integration: Connect ESG reporting with Scope 1, Scope 2, Scope 3, PCF, CCF, LCA, EPD, CBAM, CCTS, and product-level carbon disclosures.

- Audit-Ready Evidence Management: Maintain source documents, assumptions, calculation logic, emission factors, data owners, approvals, and version history.

- Expert-Led Implementation: A team of sustainability, carbon accounting, regulatory, and industrial manufacturing specialists.

The Measure | Mitigate | Monetise framework turns compliance into a foundation for green assets. For exporters, this extends to even carbon border compliance i.e. the same emissions data for SEBI also supports CBAM reporting. Establish compliance infrastructure once, and use it across frameworks.

Ready to get you audit-ready BRSR Core assurance? Get in Touch with sentra.world before your next reporting deadline.